.svg)

Tied at the Hip

Correlation

I look forward to the day when we can pay less attention to traditional markets, but that day is not today. Crypto is currently highly correlated with the equity market, which posted a strong performance in March but has since reversed aggressively. Below shows Bitcoin’s price since 2021 and its 30-day correlation with the Nasdaq. They are tied at the hip. It’s an important relationship to follow so that we understand the context around what we’re trading. Attempting to extrapolate an intraday jump in Bitcoin’s price is silly when we know that we’re just trading a version of the equity market.

Source: Tradingview

But this relationship won’t last forever and when it breaks, it could bode very well for crypto. For years, skeptics have avoided crypto due to its volatility. But YTD Bitcoin and Ethereum have traded on par with major equity and bond indices and have vastly outperformed popular names such as Netflix, Snapchat, and Facebook. As macro worries subside, where will this capital flow? I think we’re likely to see Bitcoin and Ethereum lead a rally as growth capital looks for a new home in assets with positive outlooks.

Source: Tradingview

The Fed

In our February Market Commentary, we discussed the confidence game the Fed plays. The Fed has sufficiently distorted things so that bad economic outlooks are good for public markets and vice versa. Consider the deflationary period after March 2020 when the economy was in shambles, but the public market was skyrocketing. The Fed drives public markets, and economic factors drive the Fed. When economic factors scream danger, the market expects an accommodating Fed.

Aren’t we entering a recession and isn’t GDP contracting? Maybe. And in a perverse way, this is good for risk assets. As GDP contracts and employee demand decreases, CPI will come back in line allowing the Fed to take a more dovish stance. Markets are forward-looking and already expecting 12 hikes by year-end. This leaves little room for a hawkish surprise from the Fed.

Source: Bianco Research

Crypto

This brings us to managing a crypto portfolio. It’s helpful to frame things in buckets of momentum and value. Momentum should be respected and right now momentum is down. Value is more forward-looking, and it’s beginning to look attractive.

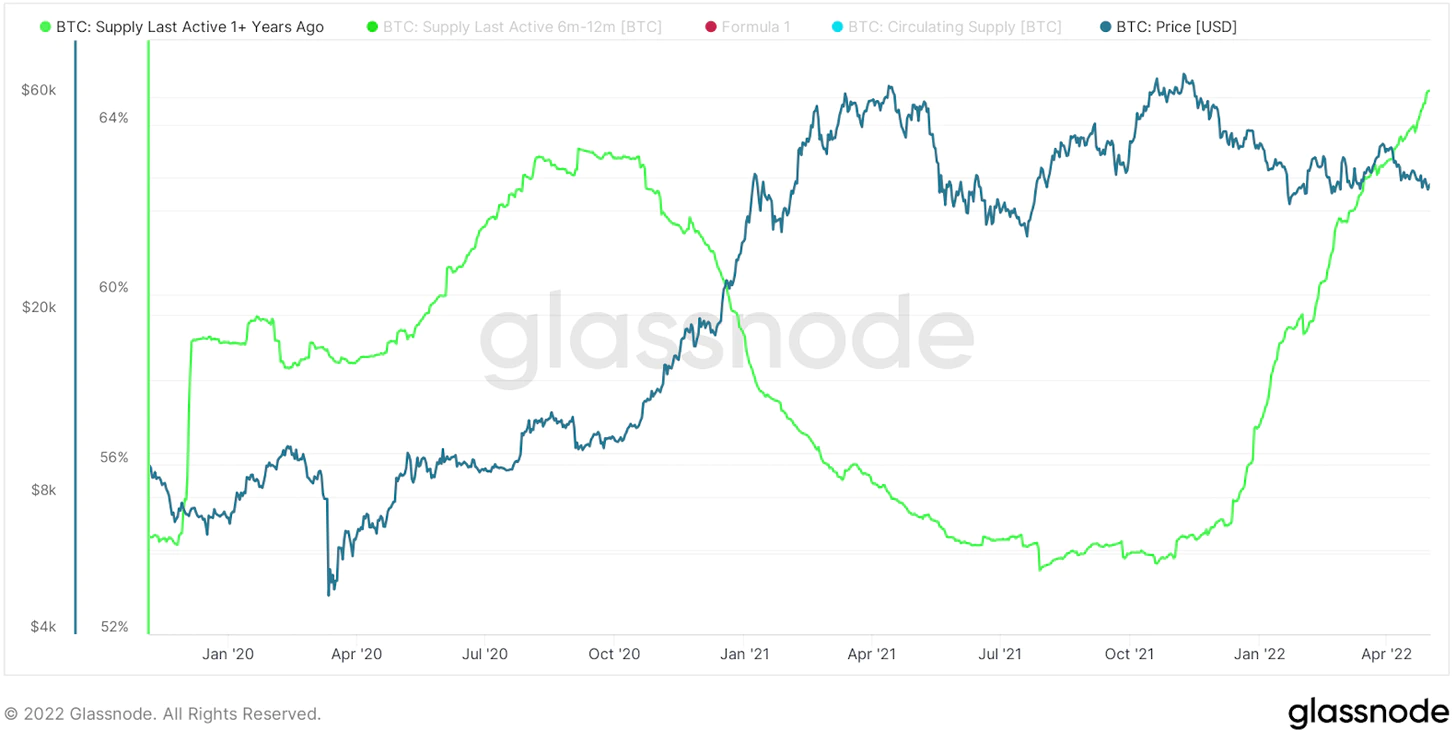

Bitcoin is an indication of general crypto sentiment and flows. Below shows that 64% of the Bitcoin supply has not moved in a year (green line). This indicates that market participants have been unphased by the market volatility and continue to accumulate Bitcoin. This isn’t a short-term indicator but one that should dictate overall bias in the next 6-12 months.

Source: Glassnode

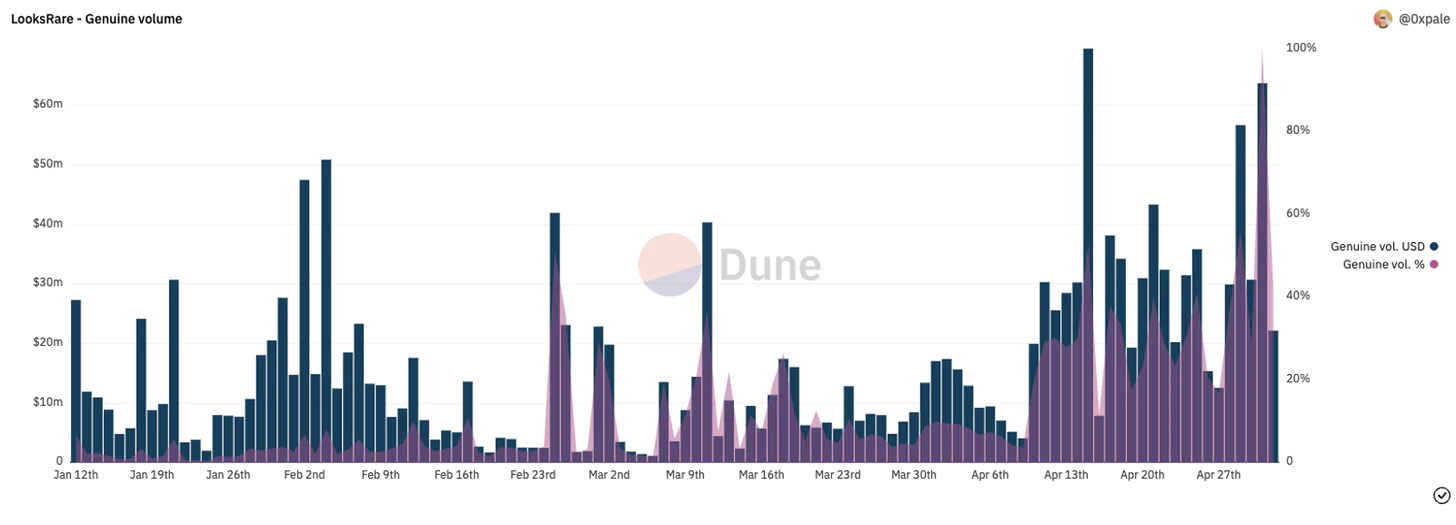

During a bull market, almost all protocol metrics look good. During a bear market, we see who’s swimming naked. NFTs have remained popular throughout the market downturn. Specific collections have fallen into deep bear markets but aggregate volume for NFTs has been elevated, nonetheless. OpenSea, LooksRare, MagicEden, and NFTX benefit from this persistent volume and may be good outlets for investing in the growth of NFTs without buying a specific collection.

Source: Dune

Source: Dune

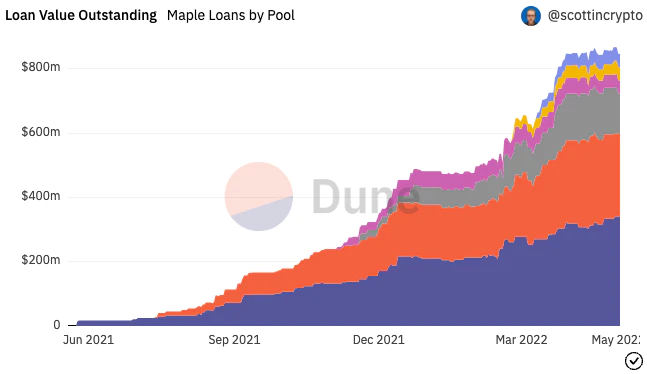

Another sector that has exhibited continued growth is undercollateralized lending, led mostly by the growth of Maple finance. As a point of comparison, Genesis Trading has a $15B loan portfolio and originated $44 billion of loans in Q1 2022. This trend is just beginning.

Source: Dune

Summary

Crypto is currently driven by overall risk sentiment. We’re in the later innings of this paradigm as cracks begin to appear in the economy leading to what could be a more dovish Fed outlook. Look for projects where growth statistics charge forward despite a slowdown in activity across the market. These have the potential to outperform amid downward momentum.

Cheers,

Plaintext Capital