.svg)

Chancellor on Brink of Bailout

Embedded in the first Bitcoin block on January 3, 2009, was the headline, “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks.” This message highlights Bitcoin’s inception as a direct response to the financial instability of the time and serves as a reminder of its importance.

Fast forward to today and Silicon Valley Bank, Credit Suisse, Signature, and First Republic Bank, among others, have faced recent crises of confidence and have highlighted bank fragility more broadly. Bitcoin has once again emerged as a possible financial refuge. Bitcoin’s significance as a bearer asset has become increasingly evident considering bank customers are now worrying about the safety of their deposits. As a self-custodied digital asset, Bitcoin allows individuals to maintain full control over their wealth, free from the potential collapse of traditional banking systems. Its bearer nature ensures that ownership and access are solely determined by possession, which in turn provides a vital layer of protection and financial sovereignty during times of economic uncertainty.

In the past two weeks, it’s become evident that the Fed and Treasury will backstop deposits to ensure trust in the banking system. However, if these deposits are indefinitely backstopped, it’s likely that we will witness another expansion of the money supply.

The Fed and central banks globally are in a tough position because inflation is still high but major cracks are forming in the banking system, and the economy more broadly. With debt-to-GDP near all-time highs, the economy is fragile. There are two options: austerity and an ensuing depression or fiscal and monetary intervention, further eroding trust in fiat monies globally.

Throughout history, austerity is rarely popular because it results in immediate pain. Currency debasement is the preferred path to dealing with debt because it happens more slowly and covertly. The Bank Term Funding Program, which we will talk about in more detail, successfully backstops banks in the short-term but will later result in monetary expansion.

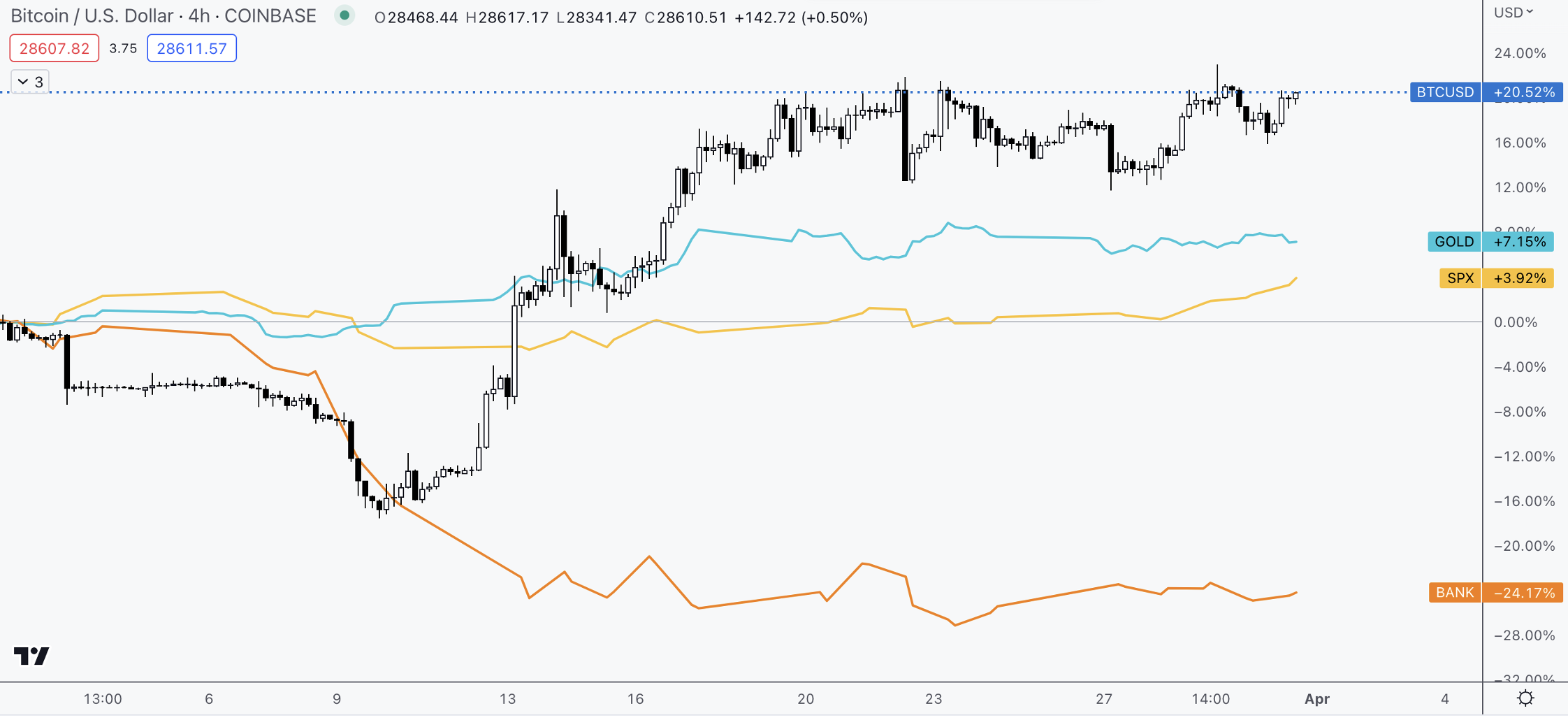

While currency debasement looms as a bleak future, Bitcoin is a much-needed reprieve, offering a decentralized and fixed-supply alternative to preserve value and foster financial stability. Bitcoin was one of the best-performing financial assets in March, moving in a similar fashion to gold but with a stronger force. Meanwhile, the BANK index was down 24% on the month.

The Bank Term Funding Program

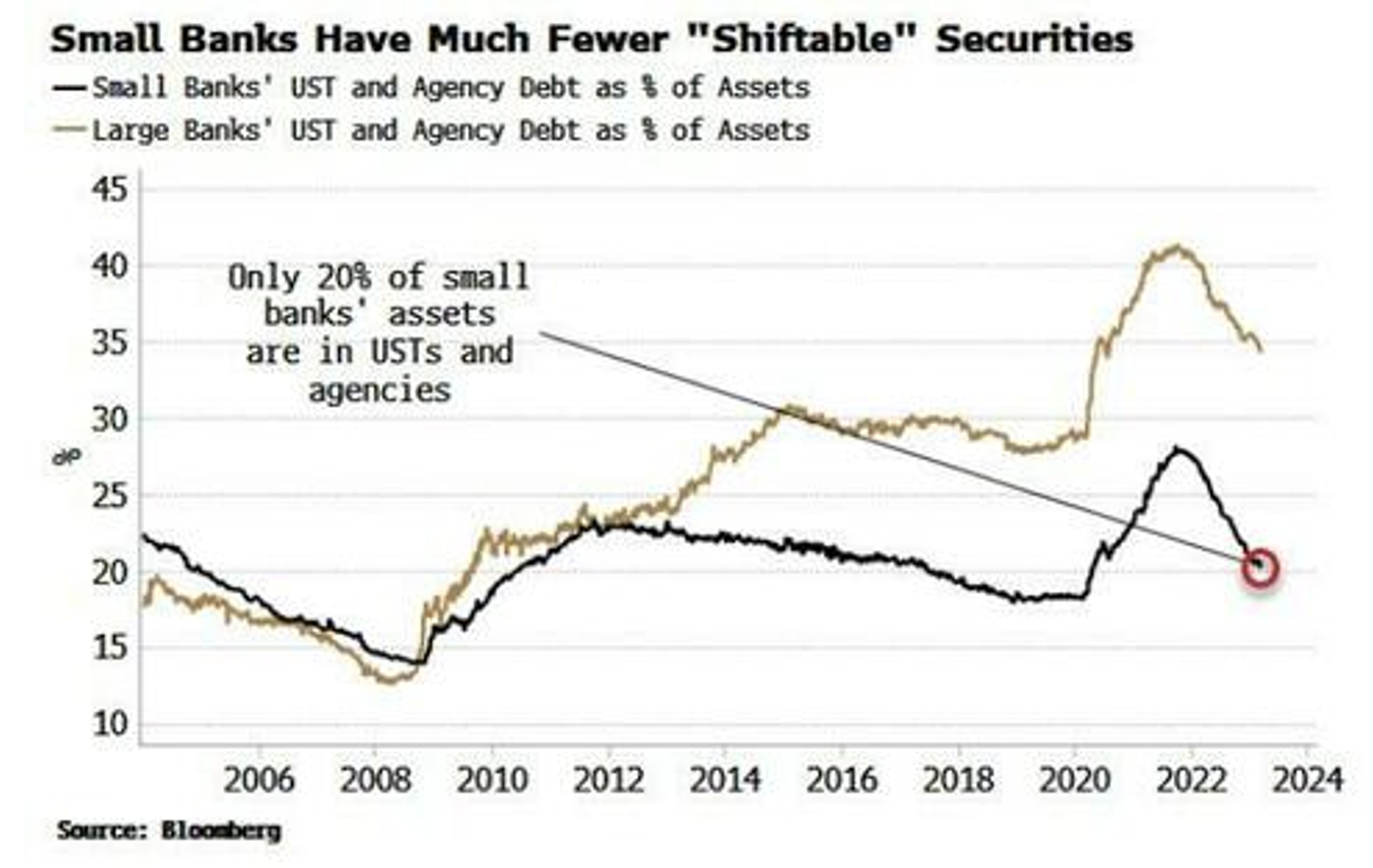

The Bank Term Funding Program allows banks to get cash by pledging Treasuries and mortgage-backed securities, which would regularly be discounted heavily in the open market, at par. This shores up $4.4 trillion in cash because that’s the par value of those Treasuries and MBSs that banks hold. The problem is regional banks don’t hold many of those securities. Instead, they hold commercial real estate loans, loans to small businesses, etc. The chart below illustrates this gap.

If small banks continue to see deposit outflows, it’s likely that BTFP will be expanded to include things other than treasuries and MBS. This could shore up another $5 trillion in cash for banks. It’s important to emphasize, that things likely need to get worse before an expansion like this would be entertained.

In the short-term, BTFP shouldn’t be stimulative to the economy or financial markets for a few reasons. First, the program is relatively expensive; banks must pay the overnight rate plus 10 BPs. Since the program is currently focused on Treasuries and MBS, loans in other areas will not be backstopped by the Fed. Also, since short-term rates are still higher than long-term rates, banks can’t make money borrowing short-term and lending long-term. Instead, BTFP serves as a safety net as credit dries up, which will be deflationary.

The program becomes interesting if the backstop is expanded to support a wider range of loans. Additionally, if inflation normalizes and the yield curve goes positive, the banks would be able to profitably borrow against what would normally be marked-down securities (at par) at a relatively attractive short-term rate and then lend out at a higher long-term rate. Typically, banks might be weary of lending in such an uncertain environment, but with a hypothetically expanded BTFP in place, the risks associated with these loans will be mitigated. The BTFP is supposed to be a 1-year program but that’s unlikely because these problems aren’t going to evaporate in a year.

The short story is that while the BTFP is unlikely to be stimulative in the short-term, it could be stimulative long-term for two reasons. First, BTFP will shore up cash for banks to issue profitable loans once the yield curve is positive. Second, the program may de-risk new loans because banks will be able to offload them to the Fed if needed. What’s most important in the short-term is that the program signals that the Fed is ready to backstop the market in creative ways. Over the past year, we’ve waited for signs of things breaking because that would trigger a response from the Fed. We got our first sign in March.

The short-term market outlook for crypto

As mentioned earlier, Bitcoin is one of the best-performing assets of the year and has seemingly responded as a hedge to the banking crisis, maintaining a tight relationship with gold. Despite the tirade of negative regulatory headlines, Bitcoin could not be derailed. Indicators confirm a defensively positioned market, which sets us up for a sustained rally.

In the last month, Bitcoin dominance has shot higher, common behavior in the early stages of a bull market. Participants flock to Bitcoin as a value play and later money trickles down the risk curve. The banking narrative is also very fitting for Bitcoin vs some of the more tech-forward crypto assets. Bitcoin is at long-term resistance at $28k-$30k and the credit contraction could cause some economic stress so while the outlook for Bitcoin and crypto is as constructive as it ever has been, liquidity conditions remain tight.