.svg)

Bitcoin's Wealth Effect

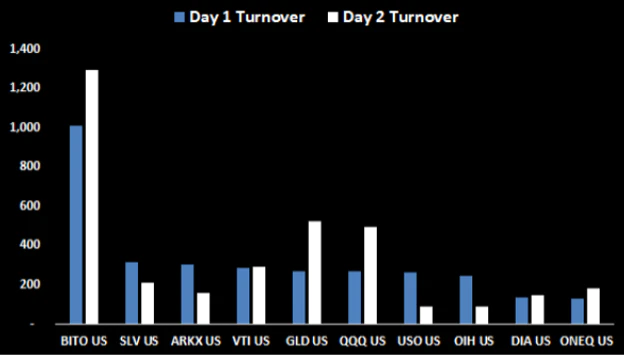

The first two Bitcoin ETFs, $BITO and $BTF launched with huge volume on October 19th and 21st, respectively. The below chart shows BITO had the largest natural volume of any ETF in the first two days of trading.

Source: Bloomberg

In tandem with the ETF launch, Bitcoin claimed new all-time highs on October 20th. Bitcoin wasn’t able to hold the highs, but we observed a common rotation play out in a few days. Bitcoin surged creating a wealth effect, demand for leverage on perpetual swaps spiked making it inefficient to long bitcoin so newly created wealth flowed from Bitcoin into higher beta altcoins, and finally, the leverage was flushed with a nearly 14% move down in Bitcoin. This cyclical flow is a crypto staple.

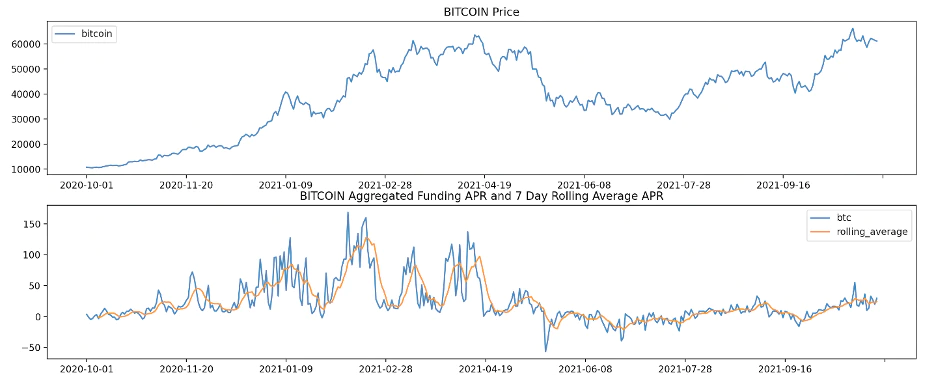

A temporary spike in leverage is often followed by a retrace but it’s generally unwise to buck the dominant Bitcoin trend. As we mentioned in the first market commentary, Bitcoin (and crypto broadly) is a uniquely trending asset because there isn’t consensus on how to value it. Because of this, price is the primary input into investors’ mental models - higher prices lead investors to forecast higher prices. And as you can see below, funding is sitting within a fairly normal range when compared to the spring.

Bitcoin’s funding rate relative to price.

Source: Plaintext Capital, CryptoQuant

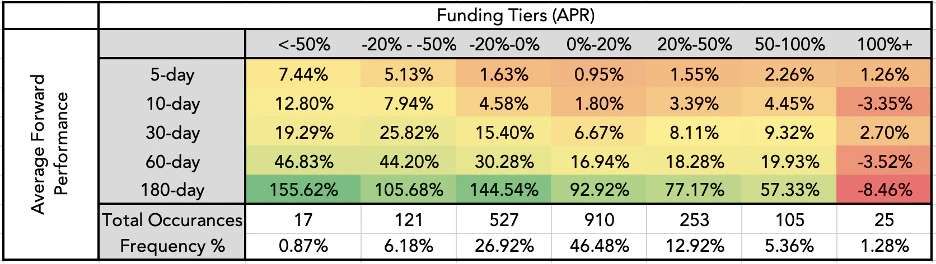

The table below shows the average forward-looking returns for each day where funding on perpetual swaps closed within a given range. We can see that Bitcoin’s forward performance remained positive (albeit decreasing) despite increases in funding, except for in rare occasions of over 100% indicative APR. The point is that mean reversion is difficult to predict, especially when Bitcoin has established a positive trend.

Source: Plaintext Capital, CryptoQuant

Market structure thoughts

Bitcoin breaking its all-time high is an important event because it revives awareness in the formation of a trend. It reminds the market that once again, Bitcoin did not die when it dropped 50%+. And now individuals and institutions alike have better access to Bitcoin than ever before. As money continues to flow into Bitcoin, it also finds its way downstream to the rest of the market. Wealth creation in Bitcoin is critical for the secular growth of the entire crypto market.

As wealth flows downstream from Bitcoin it’s helpful to consider the market structure as the population of users grows rapidly. First, there’s an obvious structural advantage to operating outside the parameters of centralized exchanges. Centralized exchanges are limited in how quickly they can add assets so using decentralized, open infrastructure allows investors to participate before a vast majority of the market. But make no mistake, centralized exchanges are rushing to add as many assets as they can to meet the demand of the ever-growing user base. Where will the tens of millions of fresh users concentrate their attention?

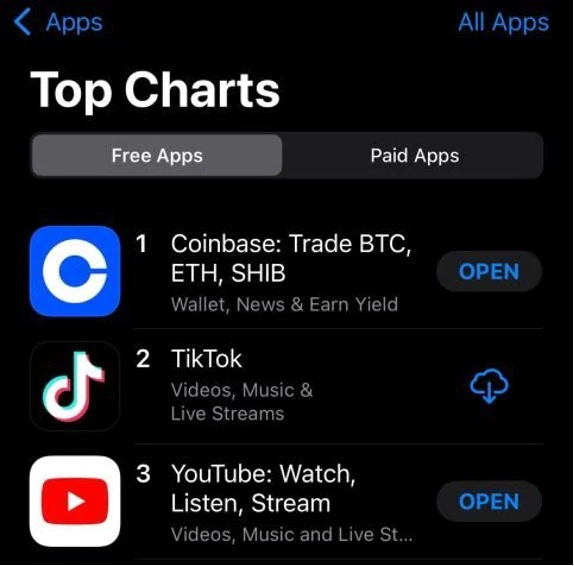

The growing retail interest for crypto is exemplified by Coinbase claiming the top spot on the App Store on October 28th. Coinbase hosts over 68 million users worldwide.

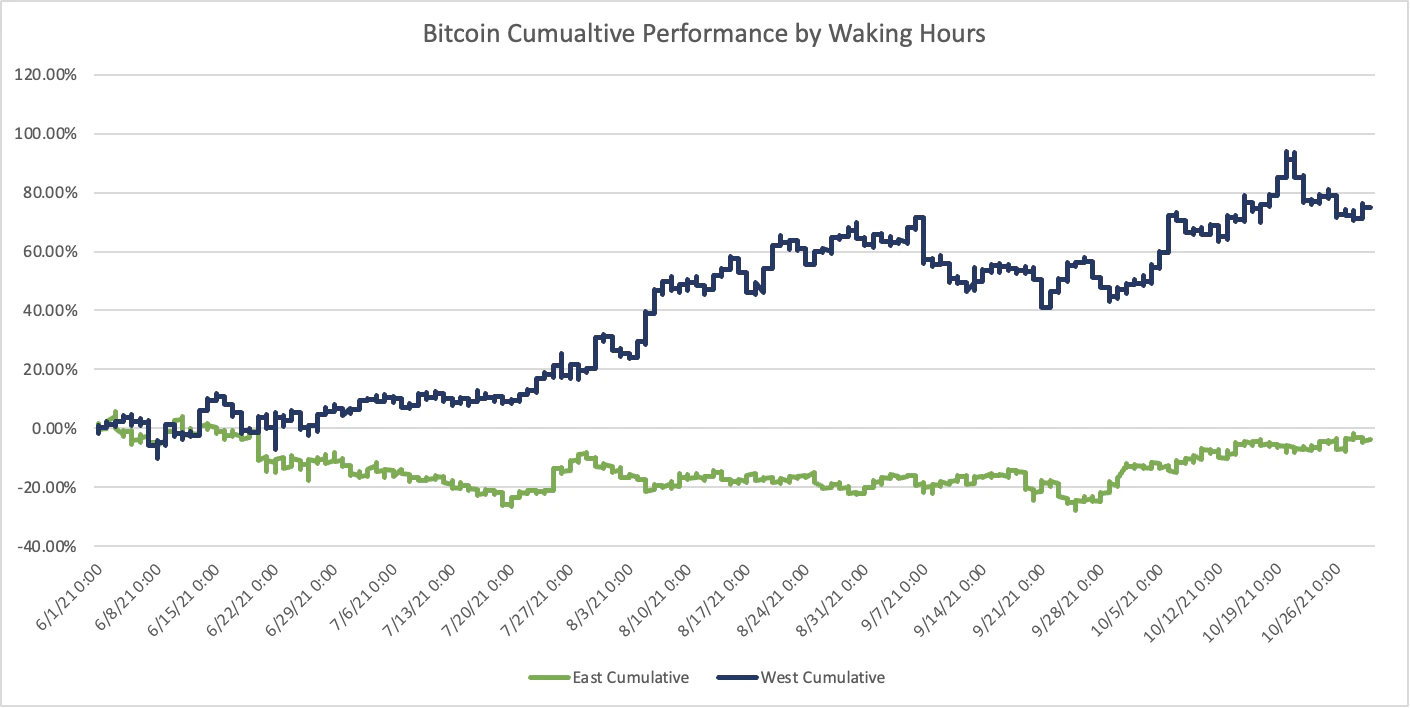

On the topic of market structure, we’re interested in understanding what buyers are driving the market. The analysis of timezones shows significantly more demand by the US over the summer, a structure that has faded since the beginning of the fall.

Source: Plaintext Capital, Glassnode

EVM battles

EVM stands for Ethereum Virtual Machine, which is a software execution environment. Ethereum is by far the market leader for decentralized applications, which gives it a considerable moat. However, blockchains that use EVM as their execution environment make it trivial to launch nearly identical Ethereum applications on another blockchain. In the last 6 months, several scalability-focused, EVM-based protocols have launched allowing Ethereum applications to easily be ported to these new protocols. Among them are Avalanche, Fantom, Arbitrum, Matic, Near, Aurora, Secret, and Binance Smart Chain.

These protocols all offer the promise of faster and cheaper transactions and are vying for the attention of users. Activity will likely funnel to a few winners but it’s unclear who those winners will be. For now, nearly all these protocols are distributing tokens to early users, helping boost interest and token prices. It’s been a profitable trend to follow but we won’t be surprised if the momentum slows when rewards run dry.

Facebook and the metaverse

Last week Facebook announced a company rebrand as “Meta” and a pivot towards building the technology needed to make a virtual universe ubiquitous. During the announcement, Zuckerberg highlighted developments in crypto and NFTs as building blocks for the metaverse. While Facebook’s reputation might not blend well with crypto’s ethos of personal sovereignty and data privacy, the announcement is validation from one of the largest companies in the world. Following the announcement, metaverse projects significantly outperformed the market as investors looked to front-run potential future integrations. Gaming and metaverse applications are likely to be a key avenue to mainstream crypto adoption.

Regulation

The SEC continues to express concern over the idea of a spot-based Bitcoin ETF, even though the currently offered futures-based ETFs are far more harmful to investors. This concern stems from spot products using market prices from unregulated exchanges. On the other hand, the underlying futures trade on the CME, a federally regulated market by the CFTC. The enormous interest in the futures-based Bitcoin ETF products is incrementally positive for spot approval but we aren’t holding our breath.

The CEO of Terraform Labs, Do Kwon, sues the SEC for unlawful service of process that transpired about a month ago during the Messari Mainnet conference. It’s clear that the SEC is beginning to take a firmer stance on DeFi products, but they appear outmatched against the thousands of products that, in many cases, operate without a central party to prosecute. Additionally, crypto firms are now going on the offense, spending huge sums to lobby for the industry’s interests. Though in the short term, SEC actions may have a considerable impact on the market.

Financial Action Task Force (FATF) published updated guidance on virtual asset service providers (VASPs). The report was expected to be harsh on the crypto industry but instead, the recommendations were balanced and left room for jurisdictions to make their own determinations.

The President’s Working Group on Financial Markets published a report on stablecoins that examines the risks and makes recommendations on how to mitigate them. The report is balanced and calls for stablecoin issuers to become banks. Additionally, custodians would have added regulatory oversight in dealing with stablecoins. The report was in line with expectations and the market rallied on relief that recommendations were not overly harsh.

Conclusion

Bitcoin’s break of all-time high is a positive catalyst for the market and should set the stage for a strong end to the year. Retail interest is returning as indicated by Coinbase’s status as the top App Store app. This has significant implications for asset performance in the short term and is an important signal for where we are in the market. Following Facebook’s announcement, we’re likely to see additional companies looking to build the metaverse on crypto infrastructure – it’s very exciting but the sector will take a long time to materialize. Finally, the regulatory environment is not overtly negative allowing the market breathing room. We feel confident in the state of the market heading into the end of the year.

Best,